Charitable Giving & Philanthropy

Giving to a charity in your Will can be a straightforward process involving an outright legacy. The good news is that the legacy should be exempt from IHT due to the charity exemption. It’s important, however, to ensure that suitable provisions are included in the Will so that if the charity is no longer in existence at the date of death, or if it has merged with another charity by that time, the gift does not fail.

Larger Estates

Testators, with larger estates, say over £1 million, on which IHT will be payable on death, may be interested in taking advantage of the reduced rate of IHT. This is a special rate of 36% (compared to the normal 40%) which is available if the testator gives at least 10% of their net chargeable estate to charity. This is not at least 10% of all an estate’s assets but at least 10% of those assets that are subject to IHT.

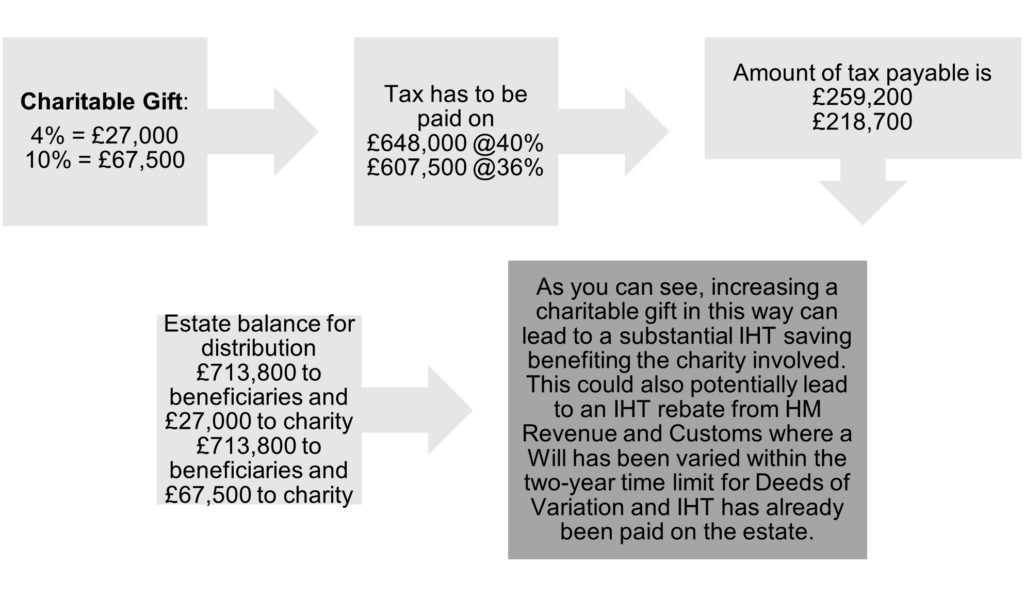

The example below shows how beneficial it can be to charities to increase an existing charitable gift of 4% of the net estate to satisfy the 10% test. Here, the gross estate is worth £1,000,000 and one ‘nil rate band’ has been deducted, leaving a net taxable estate of £675,000:

Most people’s assets go up and down in value during their lifetime so the gift can be worded so that the amount varies dependent on the size of the estate. Alternatively, the amount given can be varied by Deed of Variation within two years of death to increase the amount given to the 10% threshold provided all the residuary beneficiaries agree. In some cases, the consequent reduction in IHT can leave both the residuary beneficiaries and the charity better off.